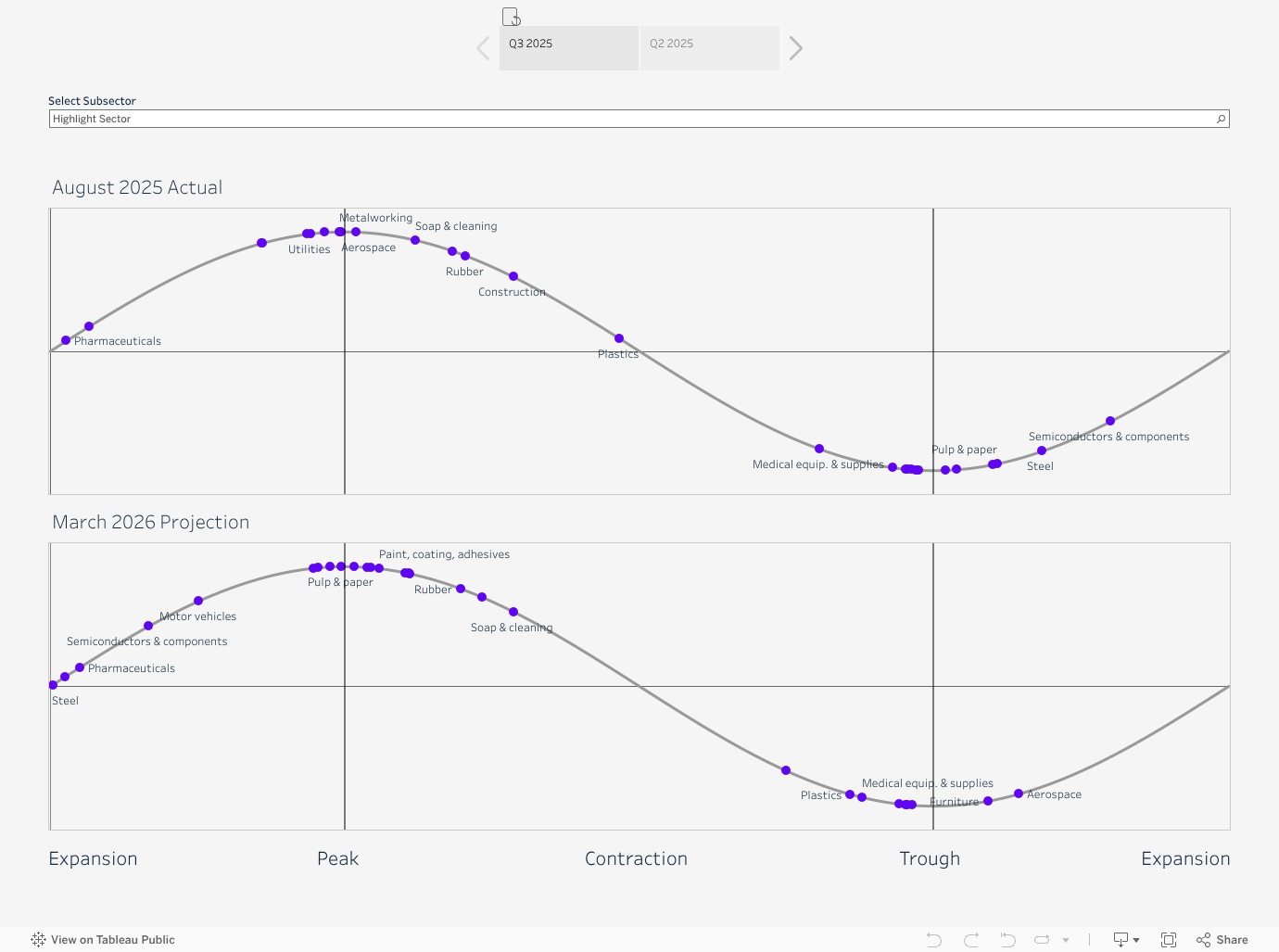

U.S. Manufacturing Subsector Business Cycle Graph

Manufacturers Alliance and Oxford Economics create this quarterly graph to illustrate where different subsectors in manufacturing currently are in their business cycle. The chart below shows their status as of Q2 2026.

Highlights from the Current Data (Jun. 2026)

- Manufacturing growth has broadened across a wider range of industries, although aerospace, semiconductors and electronic components, and increasingly, machinery continue to lead the expansion.

- After several years of stagnation, metal products manufacturing has accelerated, supported by robust demand from durable goods industries—including aerospace, motor vehicles, and machinery—which have also experienced stronger production growth and improving outlooks.

- Construction-related manufacturing remains comparatively weak, with subdued construction activity continuing to weigh on demand for building materials such as lime and gypsum products, wood products, and other construction inputs. Furniture production, which relies on housing demand is also subdued.

- Food and beverage production experienced a modest slowdown as cost-conscious consumers temporarily pulled back on spending.

- Oil and gas extraction is expected to expand moderately as higher energy prices encourage increased production to meet stronger demand following the Middle East supply disruption.

Forecast for Next Six Months (Dec. 2026)

- Most manufacturing industries are expected to remain in expansion, although construction-related manufacturing—including wood products and other building materials—will continue to lag amid subdued construction activity. Even so, construction appears to be approaching a cyclical trough, suggesting conditions are likely to improve.

- Utilities and electrical equipment are expected to remain in expansion, supported by continued investment in power infrastructure and data center construction.

- Motor vehicle parts manufacturing is expected to underperform the broader industry as the temporary tailwinds that fueled above-trend growth fade, returning production to a more sustainable pace.

- Chemicals and plastics remain weighed down by a mid-year slowdown in demand and are expected to approach the trough of their industrial cycle. However, both industries should be well positioned to rebound as broader manufacturing activity strengthens.

Underwriters